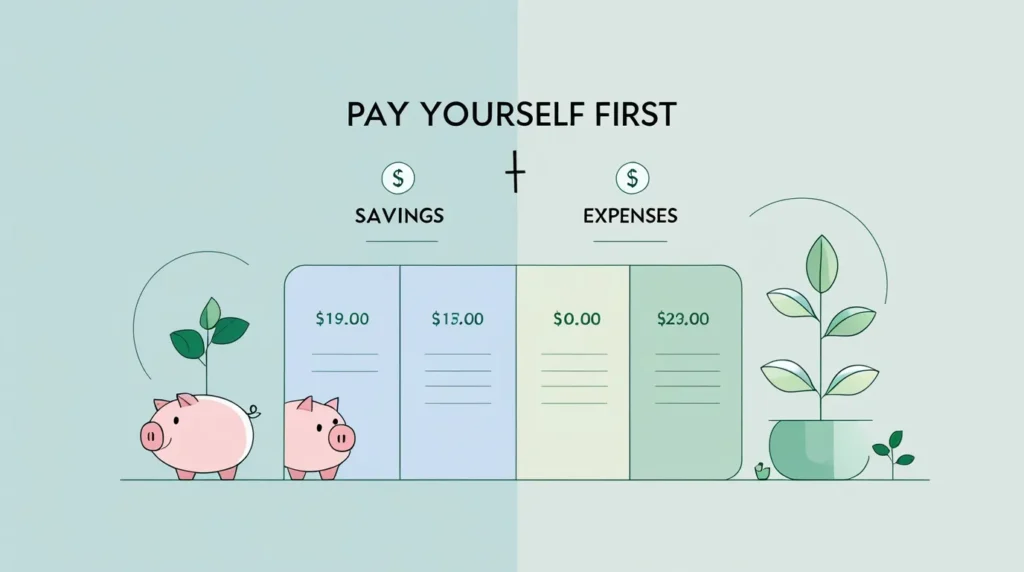

The ‘Pay Yourself First’ Principle Explained

Saving money often feels difficult because it’s treated as an afterthought — whatever remains after expenses. The “Pay Yourself First” principle flips this approach. Instead of saving what’s left, you save first and spend what remains. This simple mindset shift is one of the most powerful personal finance habits for building long-term financial security, reducing stress, and creating freedom.

What Does “Pay Yourself First” Mean?

Paying yourself first means setting aside a portion of your income for savings or investments before paying bills, shopping, or discretionary spending.

In simple terms:

Income → Savings → Expenses

(not Income → Expenses → Savings)

This ensures saving becomes non-negotiable.

Why the Pay Yourself First Principle Works

- Turns saving into a habit, not a choice

- Prevents overspending

- Builds financial discipline

- Reduces money-related stress

- Creates long-term wealth consistently

Small amounts saved regularly compound over time.

How Much Should You Pay Yourself First?

Common Guidelines:

- 10% of income (beginner-friendly)

- 15–20% for faster financial growth

- Any amount is better than nothing

Start small and increase gradually as income grows.

Where Should the Money Go?

Short-Term Goals:

- Emergency fund

- Upcoming expenses

- Sinking funds

Long-Term Goals:

- Retirement accounts

- Investments

- Wealth-building funds

Separating accounts helps maintain clarity.

How to Implement the Pay Yourself First Method

Step 1: Decide Your Percentage

Choose a realistic percentage that won’t disrupt essentials.

Step 2: Automate Savings

Set up automatic transfers on payday.

Step 3: Use Separate Accounts

Keep savings away from daily spending accounts.

Step 4: Treat It Like a Bill

Saving is a priority, not optional.

Step 5: Increase Over Time

Raise contributions with raises or bonuses.

Real-Life Example

If you earn ₹50,000 per month:

- Pay yourself first: ₹5,000

- Remaining for expenses: ₹45,000

You adjust spending habits to fit what’s left — not the other way around.

Common Mistakes to Avoid

- Waiting until month-end to save

- Saving inconsistently

- Using savings for non-emergencies

- Setting unrealistic amounts

- Not reviewing progress

Who Should Use This Principle?

- Beginners learning money management

- Salaried professionals

- Freelancers with irregular income

- Anyone struggling to save

- People building emergency funds

This principle works at every income level.

Benefits Beyond Money

- Increased confidence

- Sense of control

- Reduced financial anxiety

- Improved decision-making

- Long-term financial independence

Final Thoughts

The “Pay Yourself First” principle is less about how much you earn and more about how you manage what you earn. By prioritizing yourself financially, you create a system that supports stability, growth, and peace of mind. Over time, this habit becomes the foundation for smarter money decisions and lasting financial freedom.